From the same people who brought you the Keynes-Hayek Rap. And make sure you watch to the end.

From the same people who brought you the Keynes-Hayek Rap. And make sure you watch to the end.

It’s the subtitle that matters, Gross output will correct the fallacy fostered by GDP that consumer spending drives the economy. The actual title is “At Last, a Better Economic Measure”, it’s from The Wall Street Journal and written by Mark Skousen who has been agitating the statistical agencies in the US for around twenty years to provide just such a measure. And so now they have.

Starting April 25, the Bureau of Economic Analysis will release a new way to measure the economy each quarter. It’s called gross output, and it’s the first significant macroeconomic tool to come into regular use since gross domestic product was developed in the 1940s.

GDP is a formless mess of a statistic that was devised in the 1940s as a measure that went along with the Keynesian notion that higher spending would lead to higher employment. By embedding consumer and government spending into GDP, its put a poisoned apple into the middle of this stat so that now a shift in GDP driven by higher public spending is as misleading an indicator as it is possible to have. GDP does not measure value added although it’s supposed to and therefore does not provide much of an indication about the growth in employment-generating production. So now there is to be a new measure, Gross Output, an economic indicator that will actually provide an indication of what we are interested in knowing. As Skousen writes:

In many ways, gross output is a supply-side statistic, a measure of the production side of the economy. GDP, on the other hand, measures the “use” economy, the value of all “final” or finished goods and services used by consumers, business and government. It reached $17 trillion last year.

The measure of the economy’s gross output has been around since the 1930s. It was developed by the economist Wassily Leontieff, but he focused on individual industries, not the aggregate data as a measure of total economic activity. Gross output has largely been ignored by the media and Wall Street because the government issued the number annually, and it was two or three years out of date. That should change now that it will be released along with GDP every quarter. Analysts and the media will be able to compare the two.

Why pay attention to gross output? For starters, research I published in 1990 shows it does a better job of measuring total economic activity. GDP is a useful measure of a country’s standard of living and economic growth. But its focus on final output omits intermediate production and as a result creates much mischief in our understanding of how the economy works.

In particular, it has led to the misguided Keynesian notion that consumer and government spending drive the economy rather than saving, business investment, technology and entrepreneurship..

Misguided isn’t saying the half of it. For the first time we will have a quarterly stat that focuses on the production side of the economy and ignores the Keynesian idiocies of saying that consumer demand and government spending actually drive an economy forward. Outside the textbooks, Keynesian economics is becoming deader by the day.

Here’s a story from The New York Times via Instapundit that should surprise no one if they’ve been paying attention, The American Middle Class Is No Longer the World’s Richest. Because it is The New York Times, it is unable to understand the problem, since it puts it down to rising income inequality as the cause, but then there is hardly any major social issue it is willing any longer to discuss honestly, assuming the kinds of people who write for The New York Times any longer even have a clue what causes what. They do, however, take note of this, in a country with the largest expenditure on education per student in the world:

Americans between the ages of 55 and 65 have literacy, numeracy and technology skills that are above average relative to 55- to 65-year-olds in rest of the industrialized world, according to a recent study by the Organization for Economic Cooperation and Development, an international group. Younger Americans, though, are not keeping pace: Those between 16 and 24 rank near the bottom among rich countries, well behind their counterparts in Canada, Australia, Japan and Scandinavia and close to those in Italy and Spain.

But it’s not just the middle class who are being nailed:

The poor in the United States have trailed their counterparts in at least a few other countries since the early 1980s. With slow income growth since then, the American poor now clearly trail the poor in several other rich countries. At the 20th percentile — where someone is making less than four-fifths of the population — income in both the Netherlands and Canada was 15 percent higher than income in the United States in 2010.

But as pointed out here, the plundering of the middle class from both below and above is now standard in the US. This is not from The New York Times:

Much of America’s moneyed elite has already shifted its allegiance to the Left, especially in cities. Wealthy, educated urbanites hold generally liberal social values and can afford the higher taxes “blue” cities like Chicago impose—especially when those taxes help pay for the upscale amenities they desire. Even when the mayoral administration is less friendly, the urban elite tends to get its needs met. At the same time, the urban poor have remained loyal to the Democrats, no matter how little tangible improvement liberal policies make in their lives. And the various unions, community organizers, and activist groups that advocate for the poor profit handsomely from the moneys directed toward liberal antipoverty programs.

The US is a nation living on its capital and not its income. It will not end well.

From two articles picked up at Instapundit. First this, the conclusion to an article titled, The United States of Envy:

Voters who will hear the Obama call for envy and redistribution should ask themselves and others: Would you prefer to live in an America where the market is dynamic and opportunity abounds, or in France, where unemployment is high and tax rates are crushing? Don’t you prefer opportunity to envy?

And then this from an article with the title, Growing-ups which is subtitled, “Living with your parents, single and with no clear career. Is this a failure to grow up or a whole new stage of life’?”:

The ‘selfish’ slur also ignores how idealistic and generous-hearted today’s emerging adults are. In the national Clark poll, 86 per cent of 18- to 29-year-olds agreed that: ‘It is important to me to have a career that does some good in the world.’ And it is not just an idealistic aspiration: they are, in fact, more likely to volunteer their time and energy for serving others than their parents did at the same age, according to national surveys by the US Higher Education Research Institute.

As for the claim that they never want to grow up, it’s true that entering the full range of adult responsibilities comes later than it did before, in terms of completing education and entering marriage and parenthood. Many emerging adults are ambivalent about adulthood and in no hurry to get there. In the national Clark poll, 35 per cent of 18- to 29-year-olds agreed with the statement: ‘If I could have my way, I would never become an adult.’

Read both articles but the second shows such a high proportion of bone-headed youths who are not interested in “dead-end” jobs that you really do have to wonder about not just how dynamic the US is and but how much of that opportunity there actually any longer is.

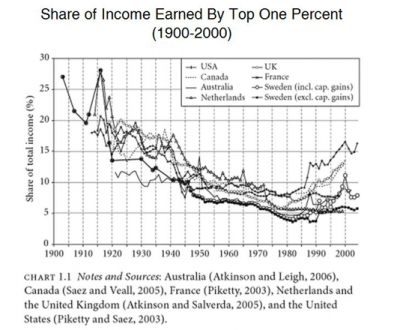

Alan Meltzer has written an article he has titled, The United States of Envy about the distribution of income across the past century. Here’s his main point:

Taxing the rich to redistribute did not produce growth. On the contrary, growth reduced the share earned by the highest earners.

Rapid growth comes from investment in new and better productive assets taking place more rapidly than existing assets are eaten away by use and decay. More saving and less consumption is what is required and nothing else will do. But here’s the catch. If investment projects are actually going to create value and raise living standards, they will have to be chosen by individual entrepreneurs – not governments who know only how to squander. Therefore, these individual entrepreneurs, to the extent they are actually successful, become wealthy. There is no way to succeed at some entrepreneurial innovation without becoming wealthy, and there is no means to organise an economy that will encourage entrepreneurial innovation without offering wealth to those who succeed. Hence envy.

But the envy is not just at wealth. No one cares about the wealth of movie stars or sports stars. They are amongst the wealthiest people in every society. But they do things that people admire and wish they could do themselves and tend to be young or at least glamorous. People who run businesses, however, are old and boring, hardworking and stodgy. Numbers people who may hire but will also fire. They focus on costs and sell what they produce at a profit. Their value system, whatever charitable work they may do and philanthropy they may spread, is still essentially Protestant work ethic irrespective of their actual religious beliefs.

But suppose it is drive, intelligence, personal ambition, an eye for detail, a grand vision and other such characteristics that matter and make all the difference. These traits are unevenly distributed across every population and thus not everyone has them to the same extent. Some people are lazy, not very bright, unambitious, slothful and without ideas, any single one of which will keep you from excelling. Well whose fault is that and why should these people be made to suffer for it? Why should the unequal distribution, not of wealth and income but of personal characteristics, determine not just your financial position but actual status in life?

So when we talk about the distribution of income we are really talking about the distribution of personal characteristics, with a tremendous amount of resentment directed towards those who actually do succeed. But what social policy has now done is to finance the lazy, the less intelligent, the unambitious, slothful and those without ideas with just enough of the earth’s worldly goods to keep them alive. But it has also vastly undermined those who might have been more ambitious, more creative, more productive with the result that individuals in great numbers fall into the abyss of non-achievement. And once in such condition, there is almost no means to pull oneself upwards. And so the envy and with it the socialism of the modern day whose greatest enemy is commercial and financial success driven by the resentment of those who can do more than they can and who are far more likely to lead lives of integrity and self-fulfilment.

Government spending absorbs national saving. Unless those resources are used in a value-adding way, the economy becomes worse off rather than better off. Spending of itself is not the road to growth. Only spending that creates more value than is used up during production leaves you ahead. We in the supposedly capitalist economies of the West are systematically ruining our economies because our governments waste our resources at prodigious rates rather than creating value or leaving those resources to be used by those who can. The United States is in the midst of turning itself into the Argentina of the twenty-first century. And as Exhibit A, let me take you to these passages from a recent column by Peter Costello, a great Treasurer because he understood these issues intuitively and with great clarity. Here he is discussing what was unmistakeable on a fight from New York to Hong Kong:

The real thing that was troubling me on that long flight to Hong Kong was why countries like the United States do infrastructure so badly when places like Hong Kong do it so well. When I flew out of New York’s Kennedy Airport, the Airtrain wasn’t working. Passengers had to bus from one Terminal to another. People were squeezed in excess of safety limits, more like battery hens than human beings. The security staff were surly and difficult. The planes were late and the terminal was rundown.

Flying into Hong Kong was like returning to the developed world. The terminal is connected to the city centre by a fast rain. Massive purpose-built suspension bridges and tunnels link it by road. Hong Kong reclaimed the land to build the airport from the sea — just as it has for other major developments.

Both these airports are owned by government authorities. Before someone tells you that we need higher taxes to pay for more infrastructure just remember that Hong Kong, with its airport and its first-class Mass Transportation System, has one of the world’s lowest tax rates, with a top income tax rate of 17 per cent and no GST.

I suspect that Hong Kong airport may be like the Moscow subway, a much more ornate facility than would be justified by the return alone and heavily subsidised as a showpiece to the world. Whether other less visible infrastructure spending in Hong Kong is equally substantial I would have my doubts. But the airport in New York is falling to bits because the capital required for mere maintenance is unavailable because so much of it is already being wasted by governments. There is an immense amount of capital in the US to get through, but Obama and the Democrats, ably assisted by the Republicans, are wasting their inheritance. Ten more years of this and it will be a poor country, as much of the country already is. There are huge lessons for us if we have the wit to understand them. I only say again that modern textbook economic theory will explain almost none of this.

Picked up at Andrew Bolt.

Judy Sloan’s column from The Australian today goes under the heading, Public spending won’t fuel the growth engine. I mention this on the same day as I have received word that my paper on Mill’s Fourth Proposition on Capital has been accepted for publication.

First Mill. In 1848, John Stuart Mill in his Principles of Political Economy included his four propositions on capital which not only never challenged in his lifetime, the fourth, that demand for commodities is not demand for labour, was described by Leslie Stephen in 1876 as the “best test of a sound economist”. It was the pons asinorum of classical economics, the divide that separated those who could understand economics from those who could not. But what is remarkable is that since that date in 1876, not only has there not been another economist to have embraced this statement in full, but it has been challenged by some of the greatest names in the history of economics – Marshall, Pigou, Hayek are just some amongst a quite extraordinary array of economists from every side of the economics divide who have tried to explain what Mill meant. To my astonishment, I am literally the first person since 1876 who has argued in print that what Mill wrote is literally true. It is the best test of a sound economist.

And what the proposition meant, as the words plainly state, is that buying non-value-adding goods and services – and here the issue is public spending in particular – will not lead to increased employment because it does not lead to economic growth. A Keynesian stimulus is therefore doomed to fail, evidence for which has been accumulating at an astronomical rate since 2009.

Judy in her column has brought forward evidence from a paper published in the UK whose subtitle is, “Government ‘investment’ does not equal growth” and written by an economist by name of Brian Sturgess. Here is Judy’s conclusion:

If the government is intent on spending even greater proportions of GDP on infrastructure — which was already ramped up under the Labor government — it must ensure that only projects for which the benefits far exceed the costs are approved. Spending money on infrastructure is no silver bullet to achieving economic growth and better living standards. Let’s just hope the audit commission has taken on board some of Sturgess’s conclusions.

Yes, let us hope our government has taken on these conclusions which once went under the collective name Say’s Law.

I put the following post up at the History of Economics list the other day because it exactly reflects a problem I am having.

I am doing some work on Keynesian economics in the period following the Global Financial Crisis. It just may be that I do not know where to look but I am having trouble finding articles of any kind criticising Keynesian models and the theory behind public sector spending and the stimulus. Can anyone help?

And as an additional query, although Mises, Hayek and Friedman are seen as “anti-Keynesian” whatever that may mean, again there seems to be a dearth of articles by them critical of Keynesian theory as it relates to public sector spending and the stimulus. So again, can anyone help?

Responses both online and offline would be greatly appreciated.

There are other economic traditions, from Austrian to Marxist, but each keeps to itself without bothering to actually criticise explicitly what they think is wrong with Keynesian analysis. And for many of the traditions, public spending in recessions is the least of their aims in changing the nature of policy based on the theories proposed. And while there have been a number of useful suggestions that have been sent to me offline as well as discussed online, there is no great cache of anti-Keynesian material anywhere that anyone has been able to unearth.

It would be one thing if the stimulus had been a no-questions-asked success, or even a mid-level so-so success, but instead it has been the most abject failure with every economy struggling to untrack from the debt and deficits the stimulus has caused. So where are the critics?

The following article on the greatest economist of the millennium was published on January 4, 2000 as one of the last of my regular columns in the Canberra Times. It was a follow up to the article on the ten most influential economists of the century that had been published two weeks before.

The Greatest Economist of the Millennium

To choose the greatest economist of the past thousand years to some extent invites the question whether the study of economics has even existed over that span of time.

Economic questions have certainly been matters of the deepest consideration for as long as humans have had commercial relations. Hammurabi’s Code, the first recorded attempt at a written system of law, sought to fix prices. Aristotle’s arguments against the charging of interest remained an obstacle to economic development for more than fifteen hundred years.

But the actual attempt to isolate an economic system from within the on-going blur of events, and then make judgements about what ought to be done, is probably no older than the sixteenth century. It was not until then that the first pamphleteers attempted to understand the structure of the economies in which they lived and to persuade governments about the policies they ought to adopt. These were the ancestors of the economists of today.

Who then was the greatest economist of the millennium? In my view it was John Stuart Mill (1806-73) whose great work, his Principles of Political Economy with Some of their Applications to Social Philosophy, was first published in 1848. There were to be seven editions during Mill’s life and it was used as a text, with few concerns about its antiquity, well into the twentieth century.

The year of publication of Mill’s Principles is one of the most significant in world history. It was the year of European revolution and in that year and for that reason Karl Marx (who is definitely not the runner up) published his Communist Manifesto. The contrasting visions of Marx and Mill were to reverberate down the succeeding years in a battle for the allegiance of the whole of the human race, a battle which has not ended even to this day.

To Marx the unit of analysis was the economic class to which one belonged. To Mill, what mattered was the individual.

The world of Marx was a world of class conflict in which the capitalist class, the owners of the means of production, exploited those who laboured but earned barely enough to keep alive.

The world as seen by Mill was strangely similar to the one inhabited by Marx, but with a recognition that an economic system based on personal liberty was one in which even those ground down by the burdens of poverty could have their material wellbeing vastly improved and their political freedoms at the same time preserved.

In one of the most remarkable passages ever written, listen to Mill’s judgement on whether the world as he knew it, if it could not be made to change, was preferable to a system in which all property was communally held.

If, therefore, the choice were to be made between Communism with all its chances, and the present state of society with all its sufferings and injustices; if the institution of private property necessarily carried with it as a consequence, that the produce of labour should be apportioned as we now see it, almost in an inverse ratio to the labour … if this or Communism were the alternative, all the difficulties, great or small, of Communism would be but as dust in the balance.

The twentieth century has been a war of ideologies in which the rights of the individual have been crushed time and again by the dictates of the state. Both the Nazis and the Communist dictatorships ruthlessly suppressed human rights in the name of a higher truth.

The cold war was fought over little more than the structure of the economic system. Massive damage was inflicted on large swaths of the world’s political landscape due to the attempts made to turn collectivist economic theories into a living reality.

Indeed, much of what is now called the third world continues to live in desperate poverty because of the introduction of central direction into their economies, an approach to solving the economic problem which has never yet worked in practice and whose continuation will guarantee poverty for so long as such attempts persist.

There is, of course, much we have learned since his time that makes Mill an imperfect guide to the operation of the economic system, although there are many worse being written even now. His theory of value, to which he believed nothing need ever be added, is the most famous instance of Mill having been superseded by the subsequent work of a later generation of economists.

Yet at the start of the new millennium, we live in the world bequeathed to us by Mill. The politics of On Liberty united with the basic propositions of his economics of limited government, free contract and individual initiative provide the blueprint for a future filled with hope and the promise of a lasting prosperity.

The following article on the ten most important economists of the twentieth century was published in the Canberra Times on December 21, 1999 just as the century was coming to an end. Economics being ultimately about influencing the political decision making process, the criterion used to frame the list was based on their influence over policy. It was no more than a personal statement but oddly or not, it was the only such list published at the time. So here they are, my list of the Ten Most Influential Economists of the Twentieth Century. And if you find this of interest, you might then have a look at my note on the greatest economist of the milennium.

Who were the century’s most important economists? The following presents my own selection of the ten economists of the past hundred years who have had the greatest influence on policy.

1. John Maynard Keynes is far and away this century’s most influential economist, but in saying this it should not be thought I believe that influence as having been for the good. Until the publication of his General Theory in 1936 it was well understood that public spending dragged an economy down rather than propping it up. It will be well into the next century before his destructive influence will have finally disappeared.

2. Friedrich von Hayek is the economist of choice for those nations who have lived under communism these past fifty years. His name today is virtually unknown in the West, but within those economies trying to resurrect free markets, his is the guidance most frequently sought. His Road to Serfdom is beloved by anyone who treasures political freedom.

3. Ludwig von Mises took the fight up to the socialist dogmas of the early twentieth century and showed on paper that no economy could ever solve the problem of allocating resources without a price mechanism, free markets and private property. Who doesn’t know it now? He knew it eighty years ago.

4. Milton Friedman has been the single most important advocate of free markets in the late twentieth century. He was also instrumental in turning the attention of governments away from Keynesian policies, which had created massive worldwide inflation, towards the need for monetary disciplines and a balanced budget. Much of what sounds like the mantra of the economics profession today Friedman had advocated almost on his own in the early years of the post-War period.

5. Arthur Pigou is in many ways my favourite. A conscientious objector during World War I, he nevertheless spent his summers as an ambulance driver on the Western Front. He also wrote the Economics of Welfare which provided the basic framework in which to consider how best to deal with harmful side effects (“externalities”) to the production process. Most of the solutions to greenhouse problems developed by economists today are based on his original work.

6. Paul Samuelson makes the list twice over. His Foundations of Economic Analysis changed the study of economics from a subject based on words into a discipline where without mathematical ability one is entirely lost. But even had he not written his Foundations, his first year text, simply titled Economics, is easily the most influential of our time, having educated three generations in Keynesian sophistries whose baneful effects are indelibly imprinted on the profession.

7. John Kenneth Galbraith wrote popular works on economics which had a massive influence in their time. His basic line was that wage and price controls are an absolute necessity if an economy is to be run at full employment with low inflation. More countries than one ended up adopting such controls whose only effects were to prolong inflation and lower employment. His books still make entertaining reading; just don’t follow the advice.

8. John Hicks was a prolific writer on a wide variety of subjects but his lasting claim to fame is based on a 1937 article, “Mr Keynes and the Classics”, in which he developed an apparatus taught to every aspiring economist. These IS-LM curves show how playing around with aggregate demand can supposedly affect the level of economic activity. It is still how almost every economist is taught to think.

9. Bill Phillips invented the Phillips curve, a device for relating the growth in prices to the growth in unemployment. Debates over policy stemming from this original model have been legion. To this day the Phillips curve sits at the core of discussions over the proper conduct of monetary and interest rate policies.

10. Robert Lucas is famed for developing the theory of “rational expectations” which explains how anticipation of the effects of government policy can prevent that policy from doing what it was intended to do. It is one of the standard ways used to explain why Keynesian policies never work in practice.

It has been a long century and these have been the economists whose names have mattered. Aside from ethnic and religious conflict, no controversies are as intense as those over how economies work. Wars and revolutions have been fought over nothing other than the architecture of the economic system. Passionate differences over economic matters are never ending.

Economists attempt to provide satisfying answers to the age old questions of how to organise production, who should receive how much of what is produced, and what should be the basis of this division.

A century from now the names will be different, but what may be said with certainty is this: the issues will be much the same as those we are dealing with today.