I have just on Friday night at 11:27 sent off to the publisher the corrected proofs of the 2nd ed of my Free Market Economics. And while I think of the book as a modern version of John Stuart Mill’s Principles of Political Economy, I received an email that has made me think that there is possibly a different and deeper source for the book I wrote. There is about to be The First International Congress on Jean-Baptiste Say to be held in village in near Lille called Auchy-lès-Hesdin. And why there? Because that’s where J.-B. Say lived and built his business.

But the core issue of this conference is not about Say’s Law but about the entrepreneur. That, too, is what my text is about: the entrepreneur, Say’s Law (i.e. the law of markets) and the market economy. This is from the Elgar posting on the first edition of which the second is the same only much more:

The book does more than recast macroeconomics in its classical form. The microeconomic sections of the book also provide a different perspective on the nature of the market, the role of the entrepreneur and the unparalleled importance of uncertainty whose significance in economic analysis cannot be exaggerated.

That is exactly what this conference is about. These are the abstracts of the first set of papers listed in the 48-page conference program which is part of the opening round table on “J.-B. Say and the liberation of productive forces”:

It should be remembered, first of all, that under his training as a young merchant, Jean-Baptiste Say spent two years with his younger brother Horace, near London in Croydon. In 1786, he moved to Britain to learn the practice of English commercial business. This happened in the midst of the development of manufacturing in the UK when the introduction of mechanical looms gave a great boost to the whole industrial activity. It is clear that this first experiment in an expanding industrial environment, which lasted two years, deeply influenced the young J.-B Say who was gifted with an inquisitive mind and a talent of observation. Another element that makes J.-B. Say a competent expert to analyze the economic situation in England and identify the strengths and lessons for France lies in his experience as an entrepreneur in the creation of the spinning company in Auchy (France) in 1805.

In the Traité d’Economie Politique and in the Cours Complet d’Economie Politique, Jean-Baptiste Say develops a criticism of corporations and other industrial regulations. According to him, these regulations are barriers to the entrepreneurial freedom and to the progress of arts. They are almost always tools of individual and collective oppression and at the origin of various economic, social and political ills. In this paper, we detail Say’s argumentation against corporations and show that it is part of more general framework based on the influence of institutions on the economy and of machines on commerce. His critical analysis leads us to present his conception of a necessary liberation of the forces of production, which requires the creation of a general framework favorable to the freedom to undertake and a blossoming of the forces of production (machines). These elements also constitute the foundations of his political economy.

In Jean-Baptiste Say’s economic thought, a productive fund of industrial capabilities generates the emergence of entrepreneurs, workers and scholars. However, success only ensues from the exercise of entrepreneurial capabilities. This article analyzes several classifications of capabilities formulated by J-B. Say. Our first result highlights the fact that these capabilities go beyond the scope of the enterprise and concern the development of nations. Within the enterprise, there is a clear distinction between management and administration in J.-B. Say’s analysis ― the former is connected to the capacity of reasoning, whereas the latter demands qualities connected to control and supervision. Therefore, the entrepreneurial functions relative to uncertainty, innovation or inefficiency are linked to success but are not necessary conditions for the productive activity. We conclude that J-B. Say does not share the idea of an economic convergence between nations in a spontaneous way. A policy of economic development based on industrial education and the reinforcement of entrepreneurial capabilities is a necessary condition.

In his writings devoted to monetary questions, Say studies in details monetary, financial and bank innovations which he designates by the expression “representative signs of money”. Say’s analysis on money and its representation signs is very important since it takes place in a context of major change in the monetary field. The aim of this paper is to show how, in Says’ analysis, these representative signs of money are innovations of major importance. The paper begins with an analysis of the position of the representative signs of money compared to money itself. Then it studies promissory notes, bills of exchange and banknotes. Finally, the consequences of their circulation in the economy are presented, especially on the activity of producers.

Since Schumpeter, there has been a tradition in the history of the economic thought that has placed Say’s entrepreneur in a filiation Cantillon-Turgot. The aim of this article is to show that this filiation does not exist, even if certain themes such as risk, knowledge or organization of production appear in the works of these three authors. More precisely, it is possible to find a double break between Say and his predecessors. The first one lies in the analysis of the production and the division of labor, which shows that the entrepreneur in Say’s writings has not the same role as in Turgot’s ones. The second one concerns their conceptions of uncertainty and profit, which shows that the place of the entrepreneur in the distribution of income in the writings of Say is not the same that in Cantillon or Turgot’s ones. The implications of this double break are specified in the conclusion.

Jean-Baptiste Say and Joseph Aloïs Schumpeter are two key-economists in the theory of the entrepreneur. Both assigned to the entrepreneur the role of an economic engine, moved by innovation. Moreover, both lived in periods characterized by a flow of economic and political new ideas (Say: the French Revolution, the Empire of Napoléon, the Bourbon Restoration, the first industrial revolution; Schumpeter: the two World Wars, the Bolshevik Revolution, the 1929 crisis, the second industrial revolution). Their theories, embedded in troubled times; define an individual who constantly avoids being locked in (economic, social, political and technical) routines. Nevertheless, an important point distinguishes their approaches: Say describes a real entrepreneur, while Schumpeter reduces him to an ideal type.

You can see from this that the world is turning away from Keynes and towards Say. The conference papers, if the abstracts are anything to go by are all of this depth and quality. That a serious revival of Say should happen in France is not as obvious as all that although where else. But you could learn more about the nature of an economy and good policy from Say’s Treatise, I’m afraid, than from most of the textbooks found across the world today. But there is the second edition of my own which will be available in about a month.

UPDATE: Overnight I have received an extremely kind and fascinating note which included the above picture. I hope M. Tilliette will not mind my reproducing his note:

Dear Professor Kates,

Please permit me to send you this mail.

I was born in 1930 at Auchy-lès-Hesdin in the north of France where Jean-Baptiste SAY founded a cotton mill about two hundred years ago, and 200 meters from the place where he lived with his family during 8 years (1804/1805 – 1812/1813 ).

Very probably my grand–grand father met him for building matters !

Mrs. Michelle Lapierre informed me that you will meet her son Florian very soon. It is a sympathetic information for us because here we are very much interested in the revival of the memory of Jean-Baptiste SAY.

We hope other opportunities to contact you. To-day, please find here attached :

– the translation in french of your positive review about the recent book of Professor Evert Schoorl. Pr. Schoorl was happy to send me your review and I translated it for people here.

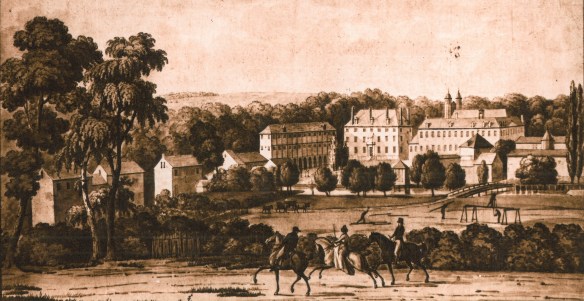

– a view of the cotton mill of Auchy around 1820 / 1825, practically as J-B SAY knew it; before it was a benedictine abbey with a water mill.

– a view of this cotton mill about fifty years later, rebuilt after a big fire in 1834. This factory was operated during almost two centuries, till 1990.

It would be a pleasure for us to send you other details about the J-B SAY time at Auchy-lès-Hesdin.

Dear Professor, I thank for your attention.

Yours truly,

Z. Tilliette