By this stage, if you still accept Keynesian economics as a legitimate approach to understanding how an economy works, or how to find our way out of recession, you are basing everything on authority and simple faith. It’s in all the texts, but you would think that by now there would be a growing level of dissatisfaction about the irrelevance of textbook theory for making sense of the actual events of an economy. Kevin Williamson has written an article, Economics may be dismal, but it’s not a science, which refers back to an article written by Niall Ferguson, The Rise and Fall of Krugmania in the UK. So we have a journalist quoting an historian on the uselessness of economic theory.

Economists have never in all their endeavors managed to deliver a truly useful and broadly applicable model to policymakers, which is to say a model that is prospective, connecting policy changes to real-world outcomes in a predictable, accurate, and reliable manner. Given the complexity at work, that probably is an impossible task, and the record of economists for making predictions is not good; Krugman’s record is arguably worse than average, despite his straight-faced insistence: “I (and those of like mind) have been right about everything.” Right about everything would be a very high standard for a marine biologist or an astronomer — but for an economist?

Krugman is trying to set a kind of standard of sorts, for being able to deny reality longer than anyone else. You know that Keynesian inanity about changing one’s mind when the facts change. Keynesian economics will disappear around the same time that the left gives up on socialism and we all know how long that will take. These people will just have to be ignored, in the way they are in the UK.

Economics does provide useful models, ones that really do work and you can use to frame policy. But all such models start on the supply side and revolve around the specific efforts of entrepreneurs living in a world of innovation and uncertainty. In that sense, economics is quite simple and straightforward. The trick is to get 50%-plus-one to vote for policies that make everyone prosperous by making some people quite well off.

Like so many others, I have the answers to the dilemma economic theory is now in. My answers centre around the classical economics that was the core of theory before Keynes brought ruin to the heart of economics with his General Theory. Clear as a bell to me the havoc this has caused, but there are other views as well, some of whom, according to The Economist, are put forward by other economists as part of their blogs. Here’s how I can tell that most of the bloggers and economists they focus on are absolutely wrong:

America is suffering from a shortfall of spending. Both market monetarism and the neo-chartalists are right about that. They disagree about whether the best response is monetary or fiscal. The market monetarists argue that fiscal stimulus should be redundant, because a central bank can always revive spending—if it sets its mind to it. If the Fed’s efforts have disappointed, it is not because market monetarism is wrong, but because the Fed is not sufficiently committed to the cause. [my bolding]

Of course, both monetary and fiscal are important: the imperative is to raise interest rates and cut spending. But I don’t think that’s what they mean.

See how fortunate you are to be able to come to this blog and find out what is wrong and what to do. The problem is that both central banks and government spending are diverting our very scarce productive resources into a series of wasteful outcomes that are making us progressively less wealthy. The gross stupidity of thinking that the cause of our currently slow rates of activity and high levels of unemployment is a shortfall of spending shows that the curse of Keynes is going nowhere soon.

[An article from 2011 sent to me from a friend for comment. Economics is not about to change is my only answer.]

There will be few moments in my life as exquisite as Wednesday when Peter Costello* came up to the University to launch the second edition of my Free Market Economics: an Introduction for the General Reader. It was a rare moment when the political side of my life, the academic side and my recognition of the importance of classical economic theory were brought together all at once, and was a moment I could share with my friends and family.

I may sometimes give the impression that the book is mostly about Keynesian economics and macro which is not the case at all. That is why I started it out, but the oddest thing for me was to find that as I wrote each chapter, that I harboured views that are far outside the standard textbook treatment. This starts even before we get to supply and demand, but I promise you this, by the time you finish with supply and demand you will know you are in a different economic world. Of course, there are demand-side market forces that limit the price that can be charged for a product, and forces on the supply side that put some kind of lower limit on the price. But the notion that there is a single equilibrium price for a product where two lines cross on a two-dimensional plane is unsupportable by even the most casual empiricism. As I point out to my classes, the price of a cup of coffee, starting from the $1 at the 7-11, to prices four and five times higher that are charged, all within a mile of the front door of our building, ought to make you appreciate that there is something else. I do teach the traditional S and D analysis, but my students also are made to understand that prices are not set by these two curves, but by entrepreneurs who are making decisions about their optimal pricing strategy, given all of the forces of the market that surround them. And most importantly, I do not let them forget that the information in a demand curve can never be known by anyone, ever. It is strictly for teaching purposes. Entrepreneurs in the real world have to work these things out for themselves in real time.

But if I have a villain on the microeconomic side, it is the MR=MC analysis and diagram. If economics had gone out of its way to find some means to cloud minds about what goes on in markets, I don’t think they could have come up with anything worse.

I teach Keynesian economics, of course, but I won’t teach that. You can find it discussed in my book, but it’s in an appendix. Over the years of teaching this diagram and the explanations that surround it, I found that after going through markets and then supply and demand, you would come to this and stop a class cold. Eventually some could draw the diagram and some might have seen the point, but there would not have been many. I do, of course, teach marginal analysis, but not like this. If you would like to see how I do it, as just part of the way this book is different from any economics book you know, Quadrant Online put up a few pages of the book under the heading Margin of Success.

As I said at the end of my presentation, there are three features of the book that I stress over and again: the role of the entrepreneur, value added and the crucial importance of uncertainty. Each is part of what must truly be understood by marginal analysis: entrepreneurial decision making in the face of the unknown future. And the point I make about the entrepreneur, as I said on the night, is that we now talk about market forces and the invisible hand, but the reality is that there is only one force that matters in a market economy, and that is the entrepreneur. And I don’t mean entrepreneur as in someone who innovates and causes change. I mean entrepreneur as in the captain of a ship in the midst of a storm a thousand miles from land.

_____

* For non-Australians, Peter Costello is the nearest equivalent we have to Ronald Reagan. He ran the economy for eleven of the best years economically this country ever had. Not only was the Asian Financial Crisis a non-event when every one of our major regional trading partners was in recession, but we ended up with 5-6% at the same time. And not only budget surpluses year after year, Australia was, until Labor took over, the only country in the world that had ZERO DEBT! The momentum given to the economy by Costello meant that we travelled through the GFC with hardly a ripple. Our problems have come since due to the debts and deficits Labor piled up. We will never see zero debt again in anyone’s lifetime, and will be lucky even to see our budget balanced any time this side of 2025.

I was directed to a post by Tyler Durden with the title, The Farce That Is Economics: Richard Feynman On The Social Sciences. As it happens I disagree with Feynman about the social sciences, and especially with his criticisms of economics. That it did not occur to him, or perhaps he did not even notice, that it was only since the publication of Adam Smith’s The Wealth of Nations that the world has achieved the kind of prosperity that was not even within the imagination of the most visionary man alive in the eighteenth century. Economists have learned a very great deal, which is why we have become so well off, but have also forgotten almost as much, which is why mainstream economic theory is such a disaster zone. But we still keep our eye on the functioning of markets, which if left to themselves will make us progressively wealthier in spite of everything we might do.

But Tyler goes on with his own list of economists’ sins which I not only agree are disastrous, and genuine, but happen to be dealt with, each and every one, in my Free Market Economics, the second edition which may be found here. This is more or less a list of economic concepts that economists have managed to unlearn over the past half century. Indeed, it is because he can see how wrong these are that he can even put together this list.

Saving money is a sin and should be penalized; speculation is a virtue and should be encouraged

The government does not need to run its finances like every other company and individual in the country; what is good for the latter is bad for the former

Inflation should be kept at 2% forever; that’s the exactly right number, no more, no less; if you start paying less for your food, rent and healthcare, the central bank must intervene

Those who take personal risks to create prosperity and jobs have obligations; everyone else has rights

The state can spend its citizen’s money much more intelligently than they can

Business cycles are bad so we must always stimulate the economy

When a boom in demand pursuant to a boom in credit inevitably fades away, we should create another boom in credit to revive demand again, and again, and again

Creating debt at a rate above an economy’s incremental productive capacity generates wealth

Anyhow, debt does not matter because that liability is someone else’s asset

Demographics don’t matter either

You generate so much prosperity in your job over 40+ years that you can comfortably live in your retirement of 20+ years

Foreign lenders only need to be concerned with regard to banana republics; the others will always pay them back

The capital markets follow nicely shaped probability bell curves, and so shocks and crashes are extremely rare events; the markets are “efficient”

The benefits of free trade outweigh the costs of a country losing its manufacturing sector as a result; the fact that domestic companies have to comply with much stricter and costlier regulations than their foreign competitors is of no consequence

Human behavior is governed by mathematical equations and models, even when oversimplifying assumptions are used

The next generation will figure out a way to pay for all the massive debts that we are creating today; otherwise the central banks will solve the problem

The way to create prosperity in a society is to take away resources from the productive sector and distribute them amongst the unproductive sector

We all admire the free markets; we just can’t let them work

The missing ingredient from economics today, as I often mention, is value added, the central concept surrounding Say’s Law. No economics text ever mentions value added outside a brief discussion of the national accounts, and I actually think very few economists, although familiar with the phrase, have any idea what it means or why it matters. If they did, they could not possibly have endorsed the stimulus, and Keynesian economics in all its forms would now be dead.

At the start of this government, Ed Miliband predicted a jobs armageddon — austerity would inevitably mean mass unemployment. Osborne would cut 500,000 public sector jobs, he said, with ‘no credible plan to replace them’. And surely government spending is synonymous with prosperity? Boldly, he forecast a ratio: one private job would be lost for every public sector job lost — leading to the loss of ‘a million jobs in all’.

The conventional Keynesian wisdom, to which Miliband subscribed, is that government spending cuts make the economy weaker: fewer public sector workers means less money spent in the shops, so less demand, therefore more unemployment. Osborne saw things differently. What if the problem was not the supply of jobs, but the supply of willing workers? If you cut taxes on low-paid work, it becomes more attractive: more people want to move from welfare. Especially if welfare reform makes it harder to game the system.

What else would someone who learns his economics from a Keynesian text believe? So let us then go to the actual situation as it has now turned out:

In five short years, Britain has gone from having mass unemployment to jobs galore. Unemployment is falling at a rate that confounds the economists, and employers are starting to panic. Maths teachers, chefs — the list of ‘shortage occupations’ grows ever longer. Construction companies are not tendering for work in London because they can’t find bricklayers. Financially this is a headache, but economically it’s a problem of success. The Prime Minister set out to get rid of the deficit. He failed. But instead he has presided over a jobs miracle — one that economists and policymakers are still struggling to understand.

Just before the Budget was published, the latest figures came out — all of them smashing records. There are 30.9 million of us in work, the most ever. That’s an employment ratio of 73.3 per cent, the highest in history. Employment is up by 1.7 million since Cameron took power and 1.5 million of these jobs are full-time. The number on Jobseekers Allowance fell by 30 per cent last year alone and the youth claimant count stands at its lowest since the 1970s. Birmingham added more jobs to its economy last year than the whole of France; Britain is adding more than the rest of Europe. David Cameron can take credit for creating more jobs than any first-term prime minister in postwar history.

The article attributes this turnaround entirely to tax cuts. Even though he notes that the central feature of Government policy has been the “austerity” program, even the writer here, who no doubt was mis-educated on Keynesian aggregate demand, cannot see, really see, what is happening before his eyes, even though he can see the outcome. Of course taxes should also be cut, which is part of the way we reduce even the ability of governments to spend. But the diversion of our resource base into productive activities is the key.

It’s this Keynesian economics that will blind you to reality. But slowly but ever so surely it is entering the dust bin of history. Shame the same cannot be said about our economics texts which still continue with the same as before.

[And my deep thanks to DB for sending this article along.]

I have received a brief email from one of my students:

Dear Dr Kates,

First let me thank you for the emails guiding us through the course.

On a personal note, I am curious as to how and why you believe that we should beware of the Keynesian approach (theories that we all have been taught at some point). Is there a book or some articles I could read to in order to understand why the pre-Keynesian era is more relevant to our current economy?

Thank you.

Kind regards

This I can tell you is not an every-day occurrence in the life of an academic. I have now replied:

You don’t know how much you have gladdened my heart in writing to me with your query. As I try to emphasise, I do not ask anyone in an introductory course to choose which side is right and I teach both. You have no doubt which side I think is valid, but I also teach Keynesian economics as accurately as anyone I know, all the more so since I understand it so well since I have studied it for so long. Nevertheless, you may be in the only classroom in the world that is taught the other side as comprehensively as you will find in this course.

But you ask where you might find some literature on the non-Keynesian classical side. I have, as it happens, just completed an 1800-page, two volume collection of every article critical of Keynesian economics written since the publication of The General Theory in 1936. But if you are looking for what I think of as the best criticism available, the best I can offer are two articles I wrote myself, the first one written at the end of 2008 and published at the beginning of 2009 just as the various stimulus packages were getting under way. The second was a five-year review of the first article written in 2014.

Both somewhat long, but both are straight to the point and were written so they could be understood without an economics training. Given how things are going, I am not anticipating much improvement on things when I come to write the ten-year review in 2019.

Again, I thank you for your query and I hope these articles will provide you with the insight into the material you are being taught. And, let me remind you, there is also the course text which covers these same issues in greater theoretical depth.

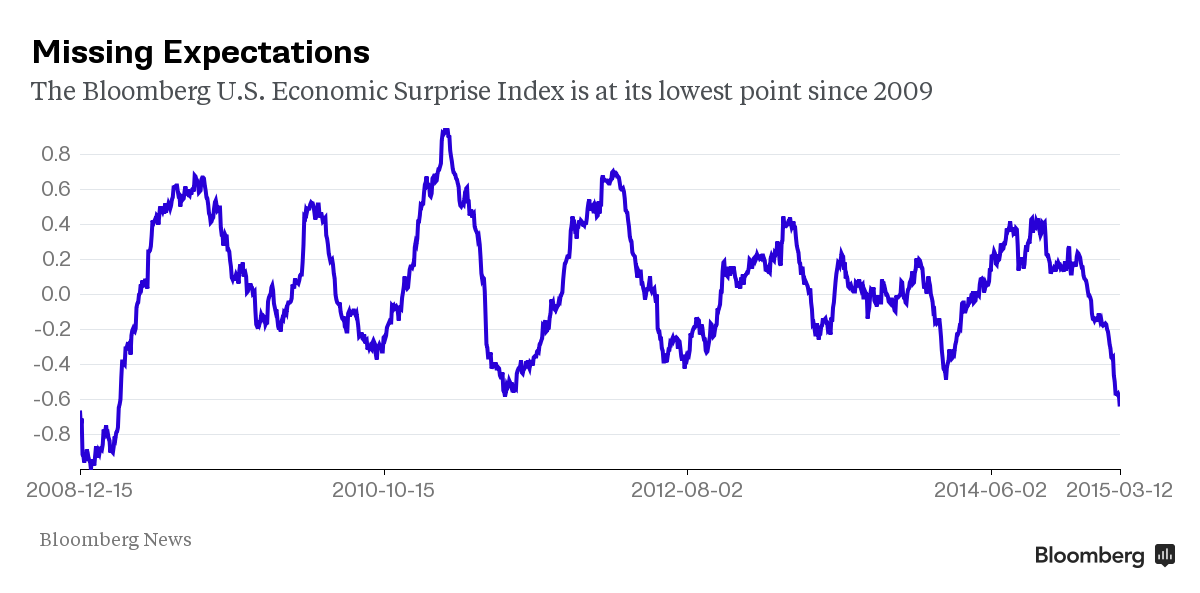

Don’t ask me what the index actually measures, but it is the worst it’s been since 2009. There is no recovery in the American economy, none at all. It is a complete mess with neither the government, the American economics community nor our existing macroeconomic texts of the slightest use in getting things back on track. This is the first para of the story from which the chart is taken:

It’s not only the just-released University of Michigan consumer confidence report and February retail sales on Thursday that surprised economists and investors with another dose of underwhelming news. Overall, U.S. economic data have been falling short of prognosticators’ expectations by the most in six years.

They however give a pass to economic management because the labour market is doing reasonably well, in their eyes. So it is useful to be reminded of the actual reality once we adjust for falling labour force participation.

The worst part is not the outcome but the lack of insight into what the problem is. Keynesian macro is an economic wrecking ball, but there is not one economist in a hundred who even has an inkling that this is so, never mind why it is so.

What our elites like most about Keynesian economics is that the wealthy get to plunder everyone else while the government can pretend it is trying to generate recovery. As the title says, For Most Of Us, There’s No “Recovery”, us in this case being in the US.

From 1820 through 2000, real (inflation-adjusted) gross domestic product grew at an average annual rate of 3.6 percent. Last year was the ninth consecutive year in which the economy grew less than 3 percent.

Real GDP has grown 13.6 percent since the recovery officially began in June 2009. The average rate of growth at this point in the recoveries from the four recessions since 1975 was 21.9 percent.

If it weren’t for gains made by the well off, there wouldn’t be a “recovery.” Five years after it began, the top 1 percent of earners (more than $366,623 a year) had garnered 81 percent of its fruits. The incomes of the top one-tenth of 1 percent (about $8 million a year) grew 39 percent.

The incomes of the bottom 90 percent declined, according to University of California-Berkeley economist Emmanuel Saez. Real median household income was $54,417 in December, 5.1 percent lower than in January 2008 ($57,317).

Most of us get nearly all our income from our jobs. Only 44 percent of adults work 30 hours or more a week, according to Gallup’s survey of the work force. Ten million fewer are working now than when Barack Obama became president.

It took until last March to create as many new jobs as were lost during the Great Recession. For every person who’s found a job, two have left the labor force.

As perhaps the only lay person in the United States to have read the two books by Sowell and Hutt, as well as Anderson’s book and some of the articles you cited in your book, I consider myself pretty knowledgeable about the logic and rationale behind Law of Markets and I must say, yours is the best I have seen on the subject.

Your classical views pretty much line up with Austrian theory, especially in their criticism of the “lack of aggregate demand” theory accepted today as being the root cause of recessions, although it would not appear that you are totally sold on their link of recessions with “expansion of money supply” and consequential “malinvestment” in production– leading to the proverbial “cluster of errors” referred to by Robbins. You seem to believe that the malinvestment can occur without the expansion of the money supply. Austrians would agree, but they would maintain that malinvestment would not cause anything but micro level adjustments or perhaps a mild slowdown and not an outright macro-recessionary period. Dispute seems to be more about degree and semantics on how to define recessions rather than serious dispute on substance. Clearly, you and Austrians do not buy the general glut argument.

Your book was excellent overview of history of economic thought, at least from early 19th C. onward. It points out how wrong Keynes was on history of economic thought, either by ignorance, or as I believe, by design. He set up a false historical narrative in developing his straw man to make it easier to take down.

Your point that the acceptance of the “lack of aggregate demand” theory by economists since 1936 has set the science of economics on a terrible path cannot be understated. Failure to understand cause will almost always result in bad policy, as can be seen by measures taken in recent years by the “policy makers”. J.B. Say: “Thus, it is the aim of good government to stimulate production, of bad government to encourage consumption”. Contrast that with:

“Simply put, we live in a world in which there is too much supply and too little demand,” star economist Nouriel Roubini of New York University …

Ugh! That is the media’s “star”. How far the profession has fallen. Unfortunately, guys like Roubini, Stiglitz and Krugman now rule the day.

I have been working on a book for several years challenging most all of modern day macroeconomic theory, with one of the first fallacies being the lack of aggregate demand theory. (The deflation bogeyman is another.) I also bought your “Free Market Economics” and just started it last night. It looks like you beat me to the punch. Keep up the good work.

Kind Regards

So today, I wrote back.

Thank you very much for your kind and encouraging letter. We are so obviously on the same wave length that it is uncanny. I had thought that once the failure of the stimulus had become perfectly clear to everyone, there would be a groundswell of some kind to think through what had gone wrong, and that, perhaps, there would be a closer re-examination of the Keynesian macro that has ruined economic theory along with most of our economies. I must therefore confess to no little astonishment to discover that Keynesian economics is even more embedded within economics than ever. I suppose that to confess to such a massive error, as would need to be done if economists rose up and said, “come to think of it, Say’s Law seems to have been right after all and Keynesian economics wrong”, would have been a gigantic step too far. But even if not that, some kind of re-thinking about how an economy works, and whether valueless public spending really can generate growth, might have been in order. Such is not how it’s been. It is therefore not a little frightening that the cures continue to be administered from the demand side.

About the way I look at the cycle, “mal-investment” gives the impression that if entrepreneurs had been more clear-eyed about the future, that the downturn would never have occurred. For me, the recession that I grew up on was the downturn that followed the OPEC oil boycott of the 1970s which was followed by a massive inflationary pulse that led to an international wage explosion. The dislocations that rolled across the world were neither caused by nor could have been cured by monetary policy. Certain categories of investment – such as those that depended on low-cost energy – were left high and dry by these major changes in the economic environment in ways that no one could have foreseen. I also think that it helps me see these things because I live in one of the more remote provinces, where domestic monetary policy will seldom be the cause of a downturn. I therefore see recessions as a consequence of government policy generally and the effects of major international instability. The GFC started in the US, and while I think we in Australia should for the most part have ignored it so far as policy went, there was never any chance we were not going to be affected irrespective of the monetary policies we might have run, either before or after. My main point is that recessions are structural and not caused by too much saving (or supply!). My chapter 14 on the cycle is a summary of the classical view, which I have synthesised from Haberler. Chapter 15 looks at the role of government, which was not a classical perspective but it is mine.

I do hope you write your own book. The one thing I know from having written what I have is that you only truly understand what you think yourself by trying to write it all down. The things that end up on the page often surprise even you. Please let me know how you go. And if I may, I will attach a paper I did on the origins of the Keynesian Revolution. Just to be able to mention Fred Manville Taylor and Harlan McCracken is often a showstopper for someone trying to argue with a Keynesian. Try it out and see how you go.

One more experiment in Keynesian economics. The politics of living within your means are what they are. The Greeks have reason to believe that they can blackmail the rest of the EU into funding their debts. But literally in this case, where will the money come from?

Syriza’s demands for a debt restructuring have raised the prospect of a stand-off between Athens and other European leaders that might lead to “Grexit” although financial markets were treating that as a marginal risk on Monday.

The potentially disastrous consequences of such a move for Greece and Europe were likely to force policymakers to find an agreement, analysts said.

So they’re beggars? So what do they care? You want to save your precious Euro, this is what you got to do? However as Daniel Hannan notes:

It would, indeed, be very difficult to make an economic case for euro membership.

The past six years have seen a greater depression in Greece than that of 1929 to 1935. Output is down by an almost unbelievable 25 per cent. A quarter of all Greeks – half of all youngsters – are unemployed, and tens of thousands more have emigrated in search of jobs.

Their currency is overvalued and market disciplines are almost invisible. If they leave the Euro, there are actually things they might be able to do.