Joe Stiglitz, that is. Here the article is on What’s Wrong With Negative Rates? But first, this admission.

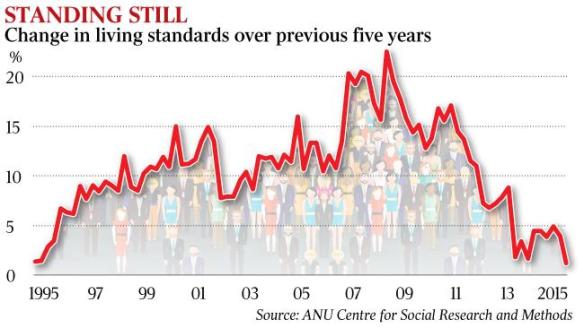

I wrote at the beginning of January that economic conditions this year were set to be as weak as in 2015, which was the worst year since the global financial crisis erupted in 2008. And, as has happened repeatedly over the last decade, a few months into the year, others’ more optimistic forecasts are being revised downward.

So even he can see that our economies are going nowhere. But why is that, you may ask?

The underlying problem – which has plagued the global economy since the crisis, but has worsened slightly – is lack of global aggregate demand.

I’m afraid that is a capital-F Fail. Wrong, wrong, wrong!!! These Keynesians don’t get it, since it never seems to dawn on them that aggregate demand can only rise if there has first been an increase in value adding aggregate supply. It’s the value adding bit in particular they don’t get, whose absence in their analyses renders everything they say about the economy completely wrong and nauseating. The are creating the poverty they say they wish to end. Hopelessly wrong on every aspect of how an economy works.

But as it happens, the article is about interest rates in particular. And as I have tried to explain time and again, as every classical economist understood, keeping interest rates unnaturally low will SLOWS THE ECONOMY AND DOES NOT SPEED IT UP. This, too, he doesn’t know, so he cannot make sense of what he sees right before his eyes. And this is what he sees right before his eyes:

In many economies – including Europe and the United States – real (inflation-adjusted) interest rates have been negative, sometimes as much as -2%. And yet, as real interest rates have fallen, business investment has stagnated. According to the OECD, the percentage of GDP invested in a category that is mostly plant and equipment has fallen in both Europe and the US in recent years. (In the US, it fell from 8.4% in 2000 to 6.8% in 2014; in the EU, it fell from 7.5% to 5.7% over the same period.) Other data provide a similar picture.

He never said don’t do it before, but now that it hasn’t worked, here it comes. He has only an ad hoc explanation for why low rates haven’t worked, but it is such nonsense that it is painful to read. You know, I do despair at such stuff. If you want to understand these things more clearly, you should go to my text, now in its second edition. If nothing else, you can at least find out what Joe doesn’t understand, why expenditures must be value adding and interest rates need to rise.